Call Us: +022 44821576

Call Us: +022 44821576

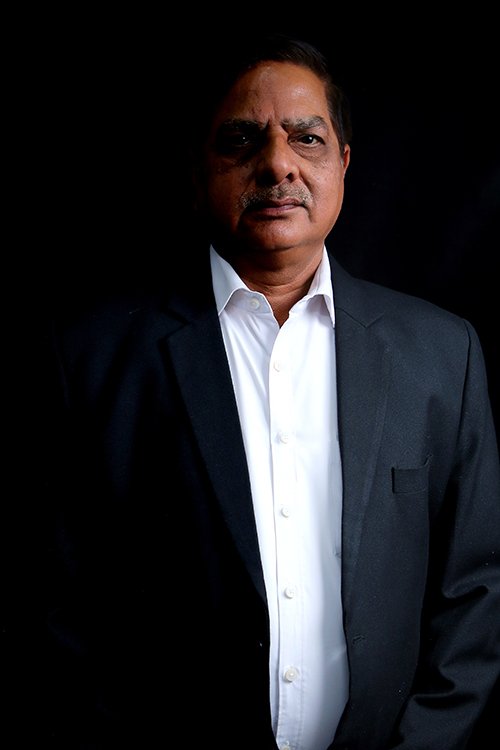

Mukesh Shrivastav is Aims Group’ Chief Financial Officer and heads the Finance & Legal functions. He brings with him over 20 years of experience in the fields of Taxation, Business Planning & Strategy, Compliance & Financial Controls, Accounting, and Audit functions. He has previously worked with “Cue Apparels”, Indian Art & Craft” He has MBA from Finance ,Law Graduate & Licentiateship from Insurance Institute of India

Electrician

Devendra Kumar has 08 years experience in electrical department .prior to joining Aims green Avenue march 2024 . He was associated with amarpali company from 2011 to 2014 and the ham square 2015 to 2017 in electrical department.

Front Desk

Rachna holds 15 Month Diploma in ADIT(Advance Diploma In Information Technology),and Pursuing Bachelors of Arts from University of Delhi, she has over 1 year of experience as an Receptionist and in Admin Field. Prior to joining AIMS in 2023 She Was Associated with IME Law College in Ghaziabad ,Uttar Pradesh.

Front Desk

Sushma Singh holds a Bachelor’s Degree in Zoology from Ruhelkhanda University, Bareilly. I have three years experience in front office, Handling the client accordingly department and entry every post received or delivery and manage all things.

CRM Executive

holds a bachelor’s degree in commerce’s From maharani college, Maharaja ganga singh university bikaner, master’s degree in MBA in HR & Marketing from Bikaner engineering college (rajasthan technical university, Kota). She has over 1 year of experience in the area of CRM .Prior to joining AIms in 2023 she was recruiter with avhm global private limited.

Legal Executive

Namit holds graduation degree in BA from shambhu dayal college ghaziabad. He has 4 years experience in the area of store. Prior to joining aims green avenue 2022 . He was associated with Gulmohar green avenue mohan nagar.

Site Incharge

Raj kumar holds diploma certificate in civil engineering from rajkiye polytechnic chandausi sambal up. He has 03 years experience in a area civil construction in India , prior to joining Aims greens Avenue 2023.he was associated with Gupta wild well maharani Bagh Delhi.

Supervisor

Anupam singh holds bachelor degree of civil engineering from Diet college of aktu.He has 01 years experience in a area architecture designing , prior to joining Aims greens Avenue 2023 November.he was associated with VMG Info services.

Site Engineer

Mujtaba Hayat Zahid holds a bachelor’s degree in civil engineering from niet college of Dr A.P.J. Abdul kalam Technical University, Lucknow he has 5 years experience in the area of civil Construction work in India. prior to joining Aims green Avenue in 2022 .he was associated with shubham builders Housing project of cpwd & pwd like itbp camp & delhi govt schools building construction & after this last company join is Parnika project of nbcc .

Project Manager

Mohammed Farmuddin Ahmad has 30years experience in fabrication & buildings interior work department ..

prior to joining aims green avenue sec-04 2020 .He was 2016 associated with Golf avenue sec-75.

Electrician

Anoop Kumar Pathak hold graducation degree in BA from Rajkiye Sthantk College pratapgarh He has 15 year experience in the area of electrical prior to joining aims green avenu 2015, He has associated with manchanda & manchanda &omax lucknow.

Jr. Bill Engineer

Er. Sonu kumari yadav holds a Bachelor’s Degree in Civil Engineering from Rajiv Gandhi Proudyogiki Vishwavidyalaya Bhopal, and Diploma Degree in Civil Engineering From RIT CSMT (BSF), Tekanpur Gwalior, and also have 3 years of experience in Civil Construction, Billing & Project Planning, Costing Estimation & Valuation, BOQ, BBS, AutoCAD 2D & 3D, Prepare Clients & Checking Contractors Bills.

Accounts Executive

Upasana butolia holds a 1 Year Computer Course – Basic, Ms Office. (Word, Excel, PowerPoint) & 6 months Tally and Bachelors commerce from Delhi University , She has over 5 years of Account experience. Prior to joining AIMS in 2023, She was associated with Outdoor communication’s Pvt Ltd in Delhi.

Accounts Executive

Richa holds 6 Month Computer Course in Basic(Microsoft Office),DTP(Desktop Publication) and have experience in Busy and Tally software and Completed Bachelors of Arts from University of Delhi, she has over 6 years of experience in Accounting Field. Prior to joining AIMS in 2023 She Was Associated with Aarvanss Buildwell and Infracon LLP in Ghaziabad ,Uttar Pradesh.

Accounts, Mumbai & MMR

Santosh Arya Holds Bachelor Degree in Commerce (Banking & Insurance) & Master in Commerce (Accounts & Finance) from Mumbai University. He has over 6 years of Experience in area of Accounts & Taxation. Prior to join Aims Promoters Pvt Ltd, he was associated with CA Firm.

Accounts Executive

Samreen holds a bachelor’s & master’s degree in commerce from CCS University, Meerut. She has over 5 years of experience in the area of Accounts.

Site Incharge

MD Junaid holds a Graduation From LNMU Darbhanga He has over 10 years of experience in the area of Executive & managing construction Prior to joining AIMS Group in 2017, he was associated with Seema Buildtech pvt Ltd & Ahuja Builders Pvt Ltd.

Site Incharge

Pramod kumar holds a graduations from ccs University meerut .he has over 13 year of experience in the area of Civil .

Admin Head

I have done B.A. from Hindu college, Muradabad, Uttar Pradesh. I am currently working as a Admin for 10 Years in Aims Group & 2 years in Vodafone as a field officer.

HR

Mariyam holds a bachelor’s degree in Science (Zoology, Botany, and Chemistry) From M.D College, M.J.P University, and master’s degree in HR & IB from AKTU University. She had over 1 year of experience in the area of human resource & management (1 year). Prior to joining AIMS in 2023.

Sr. Accounts Executive

Amit Raj holds a bachelor ‘s degree in Science from B.R Ambedkar college from Agra and also having Diploma in Financial Tally . He has over 12 years of experience in Accounts Department in Real Estate & Dairy Industries.

Sr. Accounts Executive

Prawin holds a bachelor’s degree in Commerce (Accounts – Honours) from Lalit Narayan Mithila University, Darbhanga (Bihar). He has over 20 years experience in the area of accounts in india. He has Joining Aims Group in 2006.

CRM-ASST Manager

Ashish Kumar holds a bachelor ‘s degree(B Tech) in computer science from UPTU 2010 . He has 12 years experience in area of CRM in AIMS .

Legal, Mumbai & MMR

Ravi Shrivastav, Advocate is amongst the first technology lawyers with prior qualification in Computer Science. He earned the Degree in Computer Science and Bachelors in Law (LL.B.) from the Mumbai University and a Post Graduate Diploma in Marketing from Welingkar Institute of Management Studies, Mumbai. With an exponential experience as a practising lawyer.

Ravi Shrivastav is legal advisor/consultant in AIMS Promoters (P) Ltd., proving his legal advise in drafting of legal issues, regulatory compliance, documentation of policies and contracts, vetting and review of contracts, negotiating contracts, conflict management and dispute resolution and strategic advise in managing legal issues of our company.

Ravi Shrivastav is a practicing Civil and Criminal lawyer and his work includes litigation support, litigation and non-litigation and advisory practice. He practices in the Civil Courts, District Courts, Bombay High Court and Tribunals. His work also focuses in non-litigation and advisory practice, Ravi is a legal advisor / consultant to several MSMEs and Corporates as well as Individuals or proprietary firms. His non-litigation work also includes assisting in legal and regulatory compliance, documentation of policies and contracts, vetting and review of contracts, negotiating contracts, conflict management and dispute resolution and strategic advise in managing legal issues.

Sr. General Manager & Marketing Head, Mumbai & MMR

Nishant Dilip Jain holds a Post Graduation Degree (MBA in Marketing & International Business) From Amity Institute. He has over 10 years of experience in Real estate and construction for procurements and contracts. In the past he has been associated with leading real estate groups as a free lancer for taking over and execution of projects.

Sr. General Manager & HR Head, Mumbai & MMR

Kiran Kumar is a commerce graduate and has mastered in NSD (National school of Drama). He has over a decade of experience in sales and brand management and has been associated with our group from the start. He also has vast interests in film productions.

CRM-ASST Manager

I am Ashraf Zaidi, I have done MCA (Computer Science) from UPTU University Lucknow & currently Manager CRM &, Sales in Real estate Aims group last 12 Years & 3 years worked Nirala Group( Real Estate) as a Sales Manager.

AGM Liaisoning

Vargish holds a bachelor’s degree in an Information technology (information technology- honours) from NIIT DELHI and a master’s degree in Marketing & finances from S.R University. He has over 15 years experience in the area of Liaisoning & Adminstration, both in India and in Uttarpradesh. Prior to joining M/s Aims Golf town developers pvt Ltd in 2020, he was associated with M/s Prateek group and Ms Oxirich construction pvt ltd ltd (Now Oxirich construction pvt.Ltd )

Sr. Billing Engineer

Er. Man Singh holds a Bachelor’s degree in Engineering (B.Tech Civil Engineering), and Master’s degree in Engineering (M.Tech Engineering Systems & Management) from Dayalbagh Educational Institute, Agra, (Dayalbagh Deemed to be University, Agra). He has over 6 years’ experience in the multiple areas like Civil Construction, Project Management, Planning, Costing, Estimation, Billing, Valuations, Budgeting, Executions, B.O.Q, Q.S, Procurement, and Material Testing & Indenting etc. Prior to joining AIMS in 2023. He was associated with Lords Chloro Alakli Limited & RRA Project Management Pvt Ltd.

Manager-A & F

Tasleem Ahmad Chaudhary holds a bachelor’s degree in commerce from Delhi University & master’s degree in commerce from CCS University,Meerut. He has over 14 years of experience in the area of Accounts & Finance.

V P CRM

Sandeep Sharma holds a Diploma in Civil Engineering from Lal Institute of Information Technology Faridabad and Bachelors of Arts from Chaudhary Charan Singh University Meerut, He has over 14 years of experience in the area of Civil Engineering Construction (Residential or Commercial) and Tendering, Budgeting or Costing experience Pre and Post Tendering both in India and in Bhutan. Prior to joining AIMS in 2022, he was associated with IM Cost Management Pvt Ltd in Bhutan.

Director

Amit Lohani holds a bachelor’s degree in art’s (History – Honours) From Kirori Mal College, Delhi University, master’s degree in History from Himachal University and MBA in HR & Marketing from Maharishi Institute of Management, Noida. He has over 18 years of experience in the area of human resource & managing construction (9 years). Priar to joining AIMS in 2010, he was associated with Eureka Forbes pvt Ltd.

Deputy Chief Operating Officer

Qualifications : B.com , Ll.b( Delhi University ), Jaiib( Indian Institute Of Banking And Finance ), Pg Diploma In Personal Management & Industrial Relations, Retired Agm State Bank Of India,Working In Aims Group Since 02.11.2016, Looking After Legal Matters Of The Company.

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry’s standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book. It has survived not only five centuries, but also the leap into electronic typesetting, remaining essentially unchanged.

Chief Architect & Chief Design Officer (PAN India), CEO Mumbai & MMR

Akshay is a fully chartered licensed Architect and Spatial Data Scientist with a specialisation in Real Estate. He is a fully chartered member of Council of Architecuture India and an International associate member of American Institute of Architects. He heads the Mumbai and Mumbai metropolitan region work of Aims group of companies. His real estate Experience besides Mumbai includes Delhi NCR & London.

He studied in the United Kingdom’s Ranked 1 program for Architecture at University of Bath, He did his M.Arch from University of Michigan, Ann Arbor which was then the ranked 6th program then for Architecture in the United States, He did real estate classes during his time at Michigan including some at the Ross school of Business.

He also holds an advanced degree from world renowned University of Pennsylvania where he studied Master of Urban Spatial Analytics with a specialisation in real estate for which he did classes at the Wharton School. He attended U Penn on a scholarship of 13000$ and graduated with 3.96/4.0 gpa.

Besides his role in Aims Group of Companies Akshay also runs a full fledged Architecture & Spatial Data Science consulting firm, there is some overlap between the works of the two roles, through which both companies benefit.

Outside of work Mathematics, Economics, Running and Travel interest him. He has done 27 half marathons and 3 full marathons. In class 7th in school He was the all India national rank 7 in math section of the math and science National Olympiad.

Founder & Chairperson Emeritus

Mrs. Sudha Nagar ji is the co-founder of aims group of companies. Having Studied Mathematics at Delhi University, she played a vital role in the company’s accounting and financial departments. Today she does not work in any day to day or any executive aspect of the business at all. She still holds honorary position of Chairperson Emeritus to guide the group and the team at aims group to achieve the groups broader vision and Goals. H’ble Sudha Nagar is also the Ex- District Chairperson held a diplomatic rank office, this is the highest tertiary level office or post in Govt of India at the district or tertiary level of governance.

Founder & Chairman Emeritus

Mr. Malook Nagar Ji is the co-founder of aims group of companies. He also has a successful record as an Industrialist working with leading FMCG brands in India. Today he does not work in any day to day or any executive aspect of the business at all. He still holds honorary position of Chairman Emirutus to guide the group and the team at aims group to achive the groups broader vision and Goals. A science graduate and patron of the arts he has also produced two mainstream Bollywood films, he has also served as a state legislator and was the youngest state legislator when he was elected. Malook Nagar ji is also an ex- H’ble Member of Parliament from 2019-2024.